Payment and transaction account

A payment account is an account opened by a payment service provider on behalf of one or several users and is used for the execution of payment transactions. A transaction account is a payment account opened by a bank established in Slovenia or by a branch of a Member State bank in Slovenia on behalf of one or several users. A transaction account is intended for the execution of payment transactions and other uses related to the provision of banking services. One form of a transaction account is the basic payment account, which is primarily intended for consumers who cannot open a transaction account because of (lack of) residency and/or financial standing. For the purpose of ensuring the financial inclusion of such consumers, all banks established in Slovenia that manage consumers’ transaction accounts are required to provide basic payment accounts under non-discriminatory terms. Another type of current account is the fiduciary account, which is a transaction account with a special status. A feature of the fiduciary account is that the holder opens it in his/her/its own name and for the account of third parties.

Every consumer has the option of switching a payment account open at a payment service provider in Slovenia. Switching is facilitated by the payment service provider in accordance with the Payment Services, Services of Issuing Electronic Money and Payment Systems Act (in Slovene), which sets out in detail the process of switching a payment account, the associated fees, and the responsibilities of the payment service providers involved in the switching process.

International Bank Account Number (IBAN)

The International Bank Account Number (IBAN) was introduced in response to the growing need to improve the effectiveness of the execution of payments, particularly cross-border payments. The main advantage of a standardised bank account structure is that it allows for the automatic processing of payments. In this way processed payments are executed more rapidly, at lower cost, and with significantly less possibility of error.

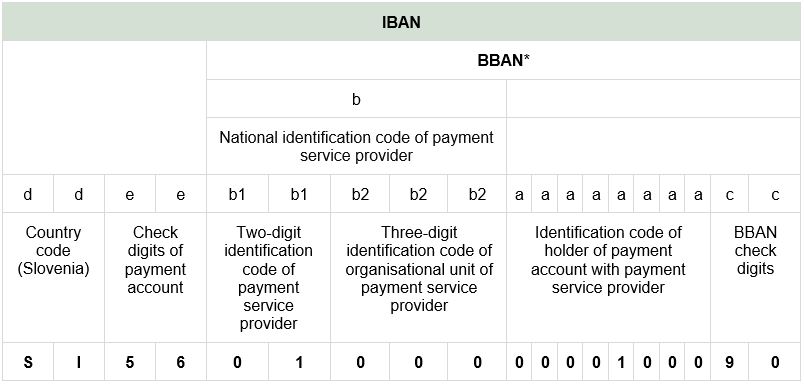

The IBAN structure is designed to allow unique identification based on which it is possible to differentiate the country of the payment service provider, the payment service provider that manages the account, and the account holder.

Illustration and example of a payment account number

* Basic Bank Account Number

The payment account number is composed of 19 alphanumeric characters, broken down into the following groups in the order prescribed:

(d) country code (Slovenia),

(e) check digits of the payment account, and the part of the payment account number that corresponds to the BBAN within the IBAN, and is broken down into the following groups in the order prescribed:

(b) identification of the payment service provider and its organisational unit,

(a) identification of the holder of the payment account with the payment service provider, and

(c) BBAN check digits.

A detailed description of the IBAN structure in each country (the IBAN Registry) can be found on the SWIFT website. Slovenia’s IBAN structure is governed by the Regulation on the content and use of the Slovenian structure of the international bank account number (in Slovene).

Register of transaction accounts

The data on transaction accounts and their holders are collected in the register of transaction accounts managed by AJPES.

The arrangement of the register of transaction accounts is defined in the Payment Services, Services of Issuing Electronic Money and Payment Systems Act (in Slovene), namely access to data or the acquisition of such data by AJPES. The data on transaction accounts of business entities are public, while the data on transaction accounts of natural persons are confidential and can be obtained by those who are entitled to them.